Contrary to revised expectations – and robust economic data – the business cycle has not been repealed. Yes, Virginia, a recession may be coming. But, like waiting for Godot, it is taking an awfully long time to arrive. If and when it does, its shape may look different, more like a mini-recession than an outright downturn. This would be akin to a soft landing – a mild slide in output accompanied by modest job losses. But suppose the weakness is pervasive and lasts more than a few months. In that case, it will nonetheless be labeled a recession by the National Bureau of Economic Research, the unofficial arbiter of when a business cycle starts and ends.

But what’s in a name? If such a Goldilocks outcome materializes and inflation is brought to heel, the Federal Reserve will gladly take it. Indeed, policymakers have been scratching their heads for some time over why the economy hasn’t yet succumbed to the most aggressive rate-hiking campaign since the 1980s aimed at taming inflation. Following more than 500 basis points of rate increases since March of last year, the economy’s growth engine has sputtered but not stalled. In fact, growth was revised significantly in the first quarter of this year – from 1.3% to 2.0%– and the preliminary look at second quarter GDP, released in late July, showed growth continued at an annualized pace of 2.4%.

While many fret that the economy is undergoing a Wile E Coyote moment – suspended in thin air and poised for a sudden and steep drop – the skeptics of the economy’s staying power are losing advocates. Earlier this year, particularly after the banking turmoil that saw the collapse of some regional banks, expectations that a recession was just around the corner ran high. Investors priced in a near 100% chance of a downturn this year, and the consensus of economists was equally convinced it would occur. Now, not so much. One reason: inflation is receding more rapidly than thought, even as the economy’s underpinnings, most notably the job market, retain considerable firepower. To many, that means the Fed can ease up on the monetary brakes, removing one headwind that is the most likely to push the economy over the cliff. Is this wishful thinking? We’ll see. It would be a historic breakthrough for monetary policy, which has usually overshot the mark in its quest to rein in inflation. But it’s also rare to see a sustained decline in inflation amid a historically tight labor market and sturdy growth. We are rooting for Goldilocks but still fear the wolf.

Still Chugging Along

Earlier in the year, most thought the economy would be on the cusp of, if not in, a recession by now. Clearly, it is not. Despite the runup in borrowing costs engineered by the Federal Reserve, tougher lending standards enforced by banks since the 9-day turmoil in March, and, until recently, slumping household confidence, consumer spending has kept the economy afloat. Retail sales did slow in June to a slim 0.2% gain, but from a robust 0.5% increase in May, that was revised up from an initial estimate of 0.3%. The bad news is that inflation rose by the same amount, so real purchases were unchanged. The good news is that the higher prices did not discourage spending, as consumers had the wherewithal to purchase the more expensive goods. At the same time, the savings rate increased to the highest level over a year, indicating that consumer incomes, not credit growth, supplement spending.

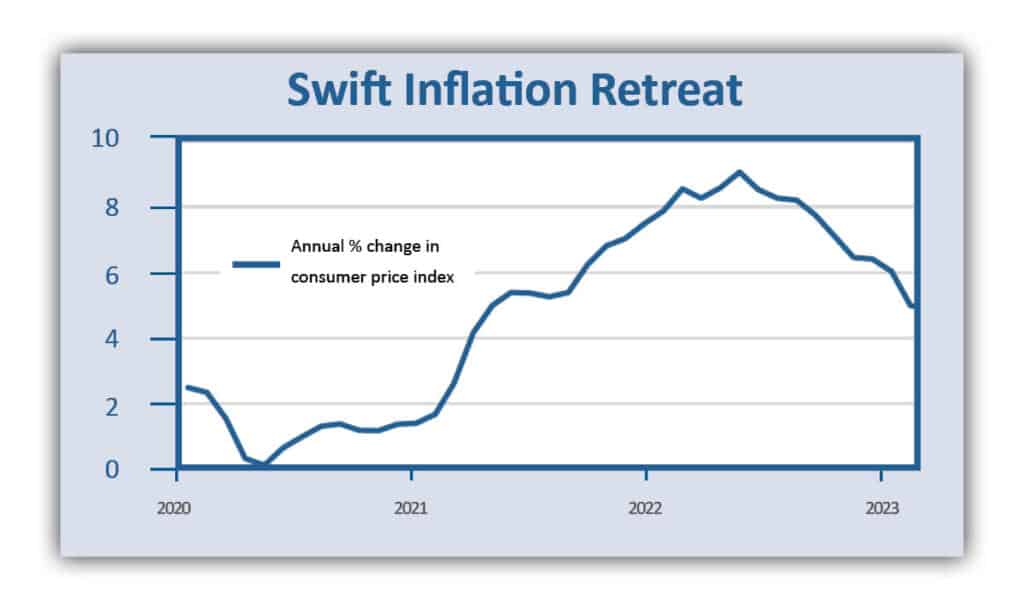

With most data for June now in the books, the economy has recorded a decent growth rate of 2.4% in the second quarter, following the 2% pace in the first. That not only puts it above recessionary waters, but it’s also about equal to the average growth rate during the ten-year pre-pandemic expansion. Does the stubborn resilience of the economy mean that the Fed’s aggressive rate hikes failed to do the job? Not if you look at the main objective of its mission – bringing down inflation. In fact, you could say it is ahead of schedule. It took 16 months for inflation, as measured by the consumer price index, to surge from under 3% to over 9%, but only 12 months to drop from over 9% back to under 3%.

Of course, this dramatic turnaround does not truly describe what happened to inflation, as the headline boomerang masks stickier prices for many of the goods and services people buy. Economists and policymakers like to exclude items whose prices are volatile to understand the underlying inflation trend better. This exercise paints an improving but less impressive disinflationary picture. The so-called core CPI, which excludes food and energy items, slowed to 4.8% in June from a peak of 6.6% last September, and prices for services, which are still in heavy demand, are rising at a 6.5% annual rate, down from an 8% peak in January.

More Work To Do

While inflation measures are improving, they are all still well above the Fed’s 2% target, suggesting that the central bank has more work to do to finish the job. Many feel that the easy pickings are over and the last mile to the finish line will be a much harder slog. That’s particularly so if the economy remains as muscular and generates hefty wage increases that businesses are pressured to pass on to consumers. But this may be a simplistic way of looking at the issue. After all, inflation has steadily receded even as the economy grew amid a historically tight job market. Why take away the champagne if the party is keeping everyone happy?

That, of course, is where the rubber meets the road. The Fed understandably believes that inflation fell despite that unforgiving backdrop because the special pandemic-era forces that propelled prices higher have unwound and punctured the inflation balloon. Supply bottlenecks that created product shortages have mostly cleared, the energy price spike from the Ukraine war shock has unwound, and the lockdown-related surge in demand for goods has ebbed as the economy reopened, prodding consumers to shift buying preferences away from physical goods to experiences. The normalization of consumer spending is still underway.

Hence, the Fed is now striving to correct traditional demand and supply imbalances they believe are keeping a floor under inflation. Most notably, they want to tame demand to bring it more in line with the economy’s output potential and to restrain job growth to bring it more in balance with the increase in labor supply. The two, of course, go hand-in-hand. By curbing demand, business revenues would suffer, and employers would likely respond by reducing labor costs – the largest expense on most balance sheets – through reduced hiring. As the job market turns weaker, so would worker bargaining positions, curbing wage demands and the pressure on employers to raise prices.

Misplaced Target?

But the argument that sustaining the disinflationary trend requires more policy tightening to squeeze businesses and labor is not overly compelling. True, rising wages put pressure on employers to raise prices. This is most evident in the service sector, which is more labor-intensive than the goods sector, which can rely more on productivity to offset labor costs. A barber can only cut one head of hair at a time, but a new machine in a factory equipped with the latest technology can increase a worker’s output — or replace the worker. (Although the actors’ strike was stoked by fears that AI replicating the image of an actor may soon do the same in the service sector).

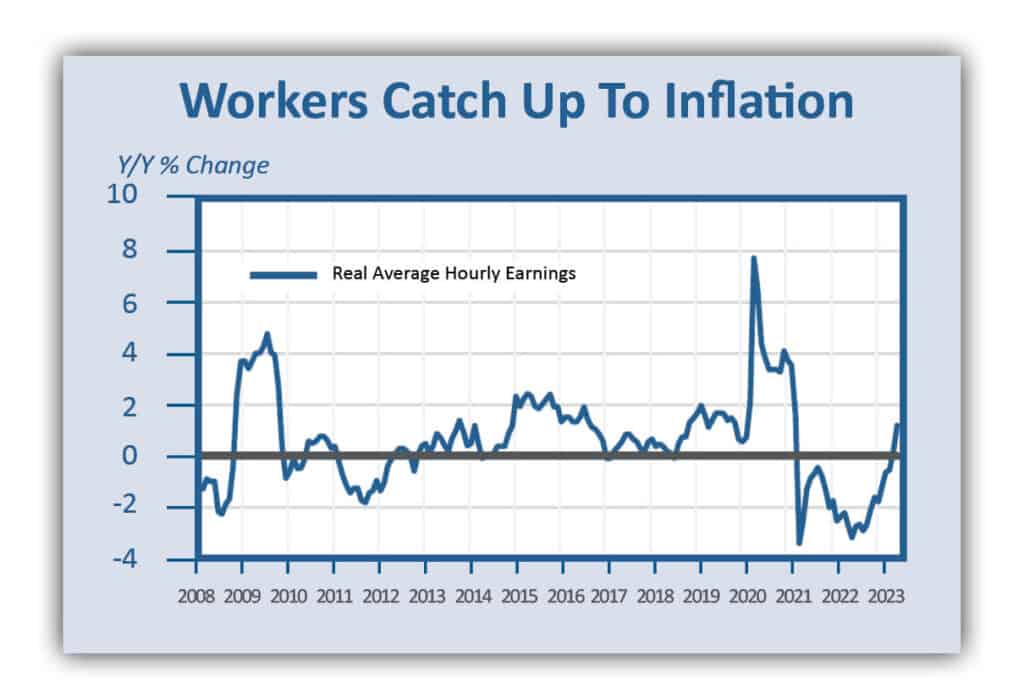

But it’s unclear how much blame for inflation should be attributed to labor costs. It is true that wage gains have finally caught up with inflation, at least by one measure of average hourly earnings compiled by the Labor Department. But rather than raising inflation – the causal input that the Fed worries about – worker pay has lagged inflation for more than two years, the longest stretch in which workers lost purchasing power since the late 1980s. That was also the last time the Federal Reserve lifted its policy rate into double digits to tame inflation and check inflation expectations by workers.

Workers have not increased wage demands this time in anticipation of higher inflation but to make up for more than two years of lost purchasing power. In fact, inflation expectations have remained well anchored throughout, so it is fair to say that wages have followed inflation, not the other way around. Hence, as inflation gradually recurs, so will wage gains, hopefully at the same or slower pace so that workers would retain the purchasing power they recaptured. Not only would a recession induced by overly restrictive Fed policy throw millions of workers out of jobs – and reverse the pay gains they achieved – it would primarily victimize lower-paid jobholders and undo the reduction in income inequality brought on by a robust job market.

Lots Of Drag In The Pipelines

When the Fed decided to keep rates steady at their June policy meeting following ten consecutive increases, they did so partly to assess past rate hikes’ impact. In the month since then, not much has changed with the economy as job growth and consumer spending have both held up well. While headline inflation, as noted, has fallen significantly, prices on a broad list of services have remained sticky. As a result, the Fed again raised rates at their July 25-26 policy meeting.

At the same time, many expect the increase to be the last of the tightening cycle, underpinning the growing sentiment that the economy can avoid a recession. A move to the sidelines would undoubtedly increase the odds that the economy can stay afloat. We fear, however, that there is enough tightening in the pipeline that eventually will push the economy into a downturn. It’s important to remember that monetary policy affects the economy with long and variable lags, and the lagged impact has yet to play out. Most of the strong data the Fed is looking at is either backward-looking or driven by forces that are poised to weaken.

Indeed, a host of time-honored leading indicators are pointing to a recession, including the Conference Board’s leading economic index, a deeply inverted yield curve, and low consumer expectations of economic conditions and buying plans. Home sales, which are always the first to succumb to a recession, are being clobbered by high mortgage rates. Some believe “this time will be different” because of the unusual pandemic-related forces behind the current business cycle. That reasoning has been invoked many times in the past but has never worked out. Recessions come and go for various reasons, and it is hard to believe this time will be any different.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

The information contained herein is for informational purposes only and does not constitute a recommendation or advice. Any opinions are those of Legacy Private Trust Company only and represent our current analysis and judgment and are subject to change. Actual results, performance, or events may differ based on changing circumstances. No statements contained herein constitute any type of guarantee, nor are they a substitute for professional legal, tax, or other specialized advice.