For the first week of the month, it looked like we were entering the time-honored “dog days of August,” the foreboding mindset people get when they feel stuck in the mud and sense things are not going right. On August 2, we saw the first signs of weakness when the Labor Department released a downtrodden employment report for July, which featured weaker-than-expected job growth and a dispiriting rise in the unemployment rate. The report spurred a hasty response in the financial markets as recession fears suddenly exploded and sent stock prices tumbling. Adding fuel to the fire, six days later, on August 8, the government agency delivered more gloomy news on the jobs front, reporting a spike in initial claims for unemployment insurance for the last week of July. Things looked grim indeed.

But after that first dispiriting week, the sun peaked out of the clouds, and things started to look much brighter. The first silver lining came again from the Labor Department in its weekly report on jobless claims. As it turns out, Hurricane Beryl had outsized effects on the late July spike in claims, as Texas businesses were hit particularly hard, causing shutdowns that temporarily sent workers to the unemployment lines. Once that unfortunate weather-related blow faded and businesses reopened their doors, firms summoned workers back, and the unemployment lines thinned out. Over the next two weeks, initial filings fell below the level that prevailed before the hurricane struck.

Unsurprisingly, the financial markets heaved a big sigh of relief, and the early losses in the stock market reversed. In the second week of August, the government released its monthly retail sales report, revealing a much stronger pace of consumer spending in July than expected and further dampening recession fears. This strong pace of spending indicated that households were not becoming frugal, as predicted by a weaker job market. We will have to wait until the September 6 release of the August employment report to see if the jump in the unemployment rate in July – from 4.1% to a three-year high of 4.3%– was a fluke. If it continues to rise, the recession worries will rise again, putting pressure on the Federal Reserve to cut rates more aggressively than is currently expected at the upcoming September 17-18 policy meeting. The Fed’s biggest challenge will be to focus on the data and avoid letting the hyper-sensitive markets influence decision making.

What To Expect if There is a Recession

Unexpected data releases spur recession calls from susceptible investors and commentators. Fortunately, the folks who are officially responsible for determining when a recession begins and ends – the experienced economists at the National Bureau of Economic Research (“NBER”) – are much more patient. They usually recognize a recession officially after its conclusion. That is because the NBER needs enough time to vet the data, which is frequently revised and not fully available until the economy is already on an upswing.

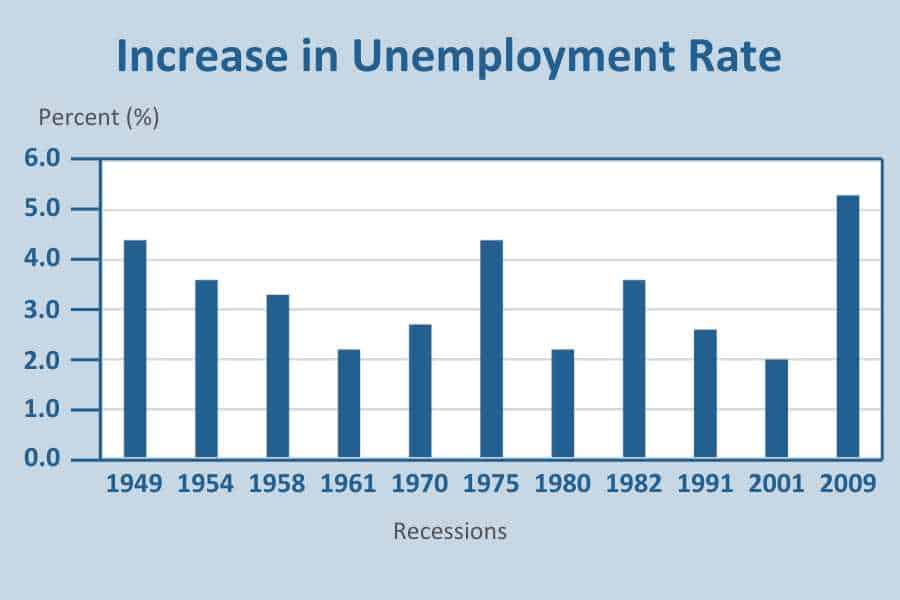

Yet, knowing what to expect if the economy does head into a tailspin is useful. No two recessions are alike, of course, but if there is one common denominator, it is that workers lose their jobs. Excluding the recession that transpired during Covid-19 – characterized by a short duration and rapid recovery – on average, the unemployment rate has risen by 3.2% over the course of the eleven postwar recessions. But the climb ranged from a mild 2.2% in 1961 to over 5.0% during the Great Recession in 2009. We omitted the spike during the Covid-19 recession because of its brevity and the rapid recovery of job losses as the economy quickly rebounded.

Still, a 3.2% rise from the 2023 low would result in a substantial 3.6 million people without jobs. The lost wages would clobber spending and dent corporate profits. That, in turn, would lead to punishing losses in the stock market and erase a chunk of the wealth gains that have contributed to the potent spending of upper-income households over the past year. That said, high stock prices and narrow credit spreads in the bond market indicate that investors are not expecting a recession soon. The markets are not always right, but recent events clearly suggest a robust economy. GDP staged an impressive 2.8% growth rate in the second quarter, with the main growth driver, consumers, forging ahead.

Hard to Stop Once it Starts

True, the recession fears that exploded earlier in the month did not come out of thin air. The July increase in the unemployment rate triggered the Sahm Rule, which states that a rise equal to 0.5% over the lowest reading of the prior year has never occurred outside of a recession since 1960. The increase in unemployment from the 3.4% low in 2023 to July’s 4.3% is still well below the 3.2% average seen in past recessions, but once it rises by that much, it is usually difficult to stop. The reason is that the economy usually enters a feedback loop at that point.

Simply put, a rise of that magnitude heightens anxiety among workers that their jobs are insecure. That, in turn, leads to a pullback in spending, which causes employers to cut back on hiring. The hiring cutback then begets a further spending retreat that leads to more layoffs, setting in motion the feedback loop that continues until the economy enters a recession. A recent New York Fed survey reveals that the percentage of workers expecting to lose their jobs over the next four months rose to the highest level since the series began in 2014.

So, are we on the cusp of another recession? Even Claudia Sahm, author of the Sahm Rule, does not think so. That is because the reasons for the current rise in the unemployment rate differs markedly from the catalysts that stoked the increase in past recessions. Namely, the current increase is not driven by massive layoffs, which would result in the lost paychecks that support spending and also stoke anxiety among workers that their jobs were at risk. Instead, the rise in the unemployment rate over the past year has reflected more labor supply coming to the job market than the demand for workers, thanks to increased immigration. These entrants are not landing jobs immediately, which is lifting the unemployment rate.

Not Out of The Woods

While it is true that a faster rise in labor supply restrained wage growth, further allowing inflation to cool is good news for the economy, but it would be a mistake to think that expanding labor supply is not accompanied by more signs of easing labor demand. Case in point, on August 21, the Bureau of Labor Services (“BLS”) unveiled a revelation that the economy generated 818,000 fewer jobs than initially estimated in the twelve months ending March 2024. Ordinarily, these annual benchmark revisions — based on more complete information than available in the monthly employment reports — are not a big story. However, this was the largest adjustment to prior data since 2009.

Since market participants already suspected that reported job gains overstated the strength in the labor market, the financial markets did not respond negatively to a jolting piece of information. Other data clearly depicted cooling worker demand by businesses as they cut job openings and laid off a large swath of temporary help. So far, however, they have retained their full-time staff, hoping demand remains sufficiently strong to justify the labor costs.

Broadly speaking, the job market is weakening but not crashing. Although the BLS revised job growth sharply lower, the unemployment rate did not change, and, despite moving up, it is still at 4.3%, which is low relative to the historical average. However, as the San Francisco Federal Reserve remarked, over the course of a business cycle, “unemployment rises like a rocket and comes down like a feather.” The opposite is happening now, but only because the economy has not entered that dreaded feedback loop described earlier. The key is to keep that prospect from happening — and that responsibility falls on the Federal Reserve.

Fed To The Rescue

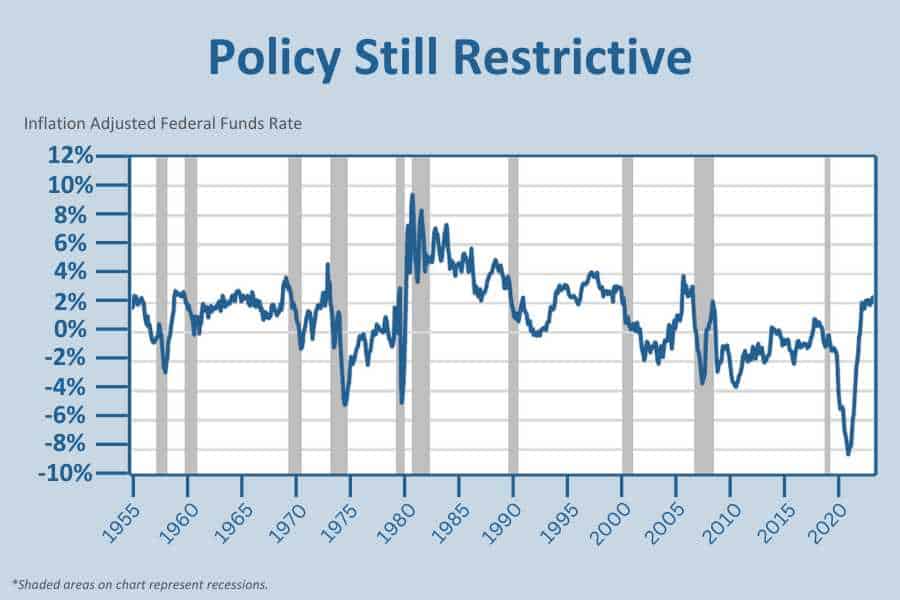

There is an old economic adage that says expansions do not die of old age, the Federal Reserve murders them. During this cycle, the Fed has done a commendable job of navigating the economy through the challenging dual mandates of price stability and full employment. Often, they have overplayed their hand to bring inflation under control, either by jacking up interest rates too rapidly or leaving them too high for too long, thus killing the expansion.

So far, the economy has weathered the steep rate climb engineered by the Fed, but the muscle that has sustained growth is rapidly losing strength. Low- and middle-income households are struggling to keep up with debt payments, exhausting their pandemic-era savings. Locking in the low prevalent rates before the Fed stepped on the brakes insulated a broad swath of the population from rate hikes. However, as those loans mature and households refinance, they will incur a higher cost associated with higher interest rates. In other words, the fabled lag effects of monetary policy are starting to kick in.

The good news is that with inflation concerns receding, the Fed can now shift their focus to sustaining job growth. At their upcoming policy meeting in mid-September, the question is not whether they will cut rates but by how much. The anticipation of a Fed pivot has been building for ten months, with the bets on Wall Street ranging from the normal quarter-point (0.25%) reduction in the Fed’s benchmark policy rate to a more aggressive – and unusual – half-point (0.50%) cut from the current median level of 5.375%. From our lens, a normal quarter-point cut is all that is necessary for the first move unless the September 6 employment report turns out to be weaker than the July report. But one thing is clear: one cut will not be enough to keep the economy out of a downturn. Even after a quarter or half-point reduction, interest rates will still be restrictive and taking an ever-greater toll on an already cooling economy. Additional cuts should be expected in the months ahead.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

The information contained herein is for informational purposes only and does not constitute a recommendation or advice. Any opinions are those of Legacy Private Trust Company only and represent our current analysis and judgment and are subject to change. Actual results, performance, or events may differ based on changing circumstances. No statements contained herein constitute any type of guarantee, nor are they a substitute for professional legal, tax, or other specialized advice.