The Federal Reserve cut interest rates for the third time in the three-month-old easing cycle that began with a robust half-point reduction in September. According to predictions made at the December- 17-18 policy meeting, the latest quarter-point cut won’t be the last. The question is, are we closer to the beginning or the end of the rate-cutting cycle? If we are still in the early stage, the next question is the ultimate landing spot—the so-called neutral rate that the Fed believes neither stimulates nor stifles growth in a stable inflation environment. Predictions of that rate are varied, which is unsurprising as it is a moving target that has changed dramatically over the years.

The Fed did announce that more rate cuts are coming, but not as many as expected a few months ago. That’s because the economy keeps chugging along, and inflation remains stubbornly higher than the central bank anticipated earlier in the year. As the notable baseball player and philosopher Yogi Berra famously noted, “It’s tough to make predictions, especially about the future.” We would add that it’s just as hard to assess what is happening now as incoming data are mostly backward-looking. Moreover, government statisticians who compile the data are coping with ever-lower response rates from the data sources. But as Fed Chair Jerome Powell has repeatedly said, we deal with the cards we have. Hopefully, the deck is not utterly misleading, resulting in bad policy decisions that can lead the economy in the wrong direction.

In addition to the central bank’s potential missteps, there is uncertainty surrounding fiscal policy. Will the taxation and spending intentions of the incoming administration be contractionary or expansionary? The proposed spending cutbacks would argue for the former, while lower taxes would say for the latter. Then there are the much-touted tariff increases, which could go either way depending on the response of trading partners. Keep in mind that the President proposes, but Congress disposes when it comes to spending and taxes, so campaign promises are not cast in stone. Simply put, speculation over monetary and fiscal policy will be a popular parlor game over the next several months, setting the stage for heightened volatility in the financial markets. The good news is that the economy is heading into the policy maelstrom with a good head of steam and is likely to exhibit the resilience it has displayed through past fogs of uncertainty.

Tough Talk on the Budget

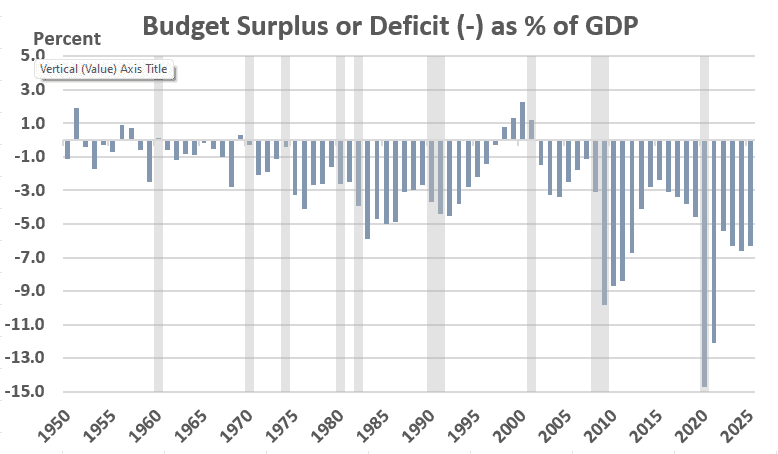

One of the incoming administration’s top priorities is to control the federal budget. The massive deficit spending since the Covid recession has sent the budget sincerely into the red. According to the latest estimates by the Office of Management and Budget, the U.S. deficit will exceed 6% of GDP in fiscal 2025 for the third consecutive year, an extraordinary share during expansions and high employment. Over the past 30 years, which includes the Great Recession and the steep but brief Covid recession, the deficit averaged less than 3% of GDP.

Scott Bessent, the nominee for Treasury Secretary, has called for slashing the deficit to 3% of GDP by the end of President-elect Trump’s second term. The incoming President has also tapped Elon Musk and Vivek Ramaswamy to jointly lead the newly created Department of Government Efficiency, commonly known as DOGE, to assist in the effort. Musk has floated the eye-grabbing figure of $2 trillion in spending cuts. Unsurprisingly, there is a growing perception that federal outlays will be significantly reined in. However, we’re not entirely buying into all the tough talk.

For one, $2 trillion in spending cuts, which would amount to a third of the federal budget, is unrealistic. During the campaign, Trump promised to protect Social Security and Medicare, which comprise a third of federal spending. Net interest on the debt accounts for another 15% of the expenditure, and interest payments cannot be missed. During his first presidency, Trump reliably requested more funding for the Departments of Defense, Veterans Affairs, and Homeland Security. It’s hard to believe that these three departments would be on the chopping block, which removes another 20% of spending from any budget-slashing effort. Simply put, two-thirds of federal spending would be off-limits. Massive cuts to the remaining third of the budget would be a tough sell for members of Congress, who, time and again, have hesitated to cut even small programs they believe benefit their constituents.

Muted Economic Impact

Nearly two months have passed since the election, and the policy landscape under a second Trump presidency remains as uncertain as ever. We suspect that the Republican-controlled Congress will squeeze some savings out of the budget but not enough to impact economic growth. Modest spending cuts will likely be offset mainly by lower taxes, rendering the fiscal impact a wash. However, the higher probability of tariff increases could be felt, particularly at higher prices.

True, the tariffs imposed during the first Trump presidency—retained mainly under the Biden administration—did not significantly impact inflation, which remained well under control until Covid hit. However, the tariffs were imposed on a far more limited scale than what is now being proposed. Many believe the aggressive tariff proposals are more of a negotiating tool to force trading partners to meet certain conditions unrelated to trade, such as tightening borders and clamping down on illegal drug trafficking. That notion has merit.

Moreover, an adverse reaction in the financial markets or the polls might also cause a reassessment by the administration. Keep in mind that someone must foot the bill linked to higher tariffs. Either companies will pass on the additional costs of imports to consumers—boosting inflation—or they will absorb the costs, leading to lower profits. Neither outcome would be favorably received by consumers or investors. Again, there is much uncertainty overhanging the policy landscape, so time will tell how the incoming administration’s plans play out.

The Other Policy Lever

To be sure, monetary policymakers will not sit idly by as events on the fiscal front unfold. The Federal Reserve, however, is in a bind. Like everyone else, they do not know what will come from Washington in 2025 and are reluctant to base policy decisions on speculation. That said, the message sent at the December 17-18 policy meeting suggests that some officials expect more inflation than otherwise due to higher tariffs and deportations that could reduce the labor supply and boost wage growth.

Hence, even as they cut rates by another quarter point at the meeting, as expected, they also signaled that they would not be lowering rates as many times next year as predicted in September, the last meeting that included a Summary of Economic Projections (SEP). The median expectation of the 19 members of the rate-setting committee is for two cuts rather than the four penciled in three months earlier. The shallower path of rate cuts was expected in the financial markets, as both economic growth and inflation were running hotter than predicted a few months ago. But investors still reacted poorly, as stock prices tumbled, and bond yields spiked in the immediate aftermath of the meeting.

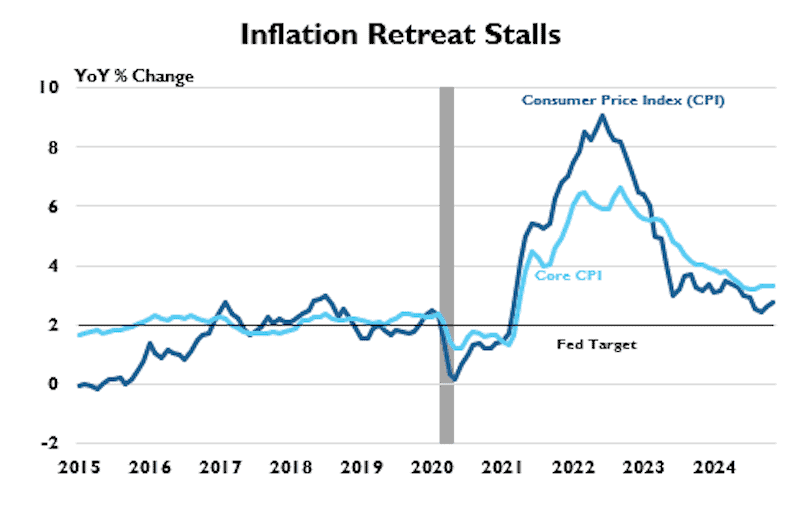

It’s unclear if the adverse market reaction was a “buy on the rumor and sell on the news” or something more profound. Curiously, the outlook for growth and employment in 2025 hardly changed from the predictions made in September. GDP was revised by 0.1%, and the forecast unemployment rate was revised down a tick from 4.4% to 4.3%. Despite the small moves in these fundamentals that drive inflation, the forecast for 2025 was revised significantly higher, to 2.5% from 2.1% in the September SEP. This implies that, subjectively at least, some Fed officials view Trump’s tariffs and proposed deportations as having an inflationary impact.

Lessons Learned

So, where do we go from here? If one thing is evident from the experience over the past several months, nothing should be taken for granted. When the Fed cut rates by a substantial half-percent in September, conditions looked dire. Many believed that the aggressive rate hikes in 2022 and 2023 aimed at curbing inflation would, in time-honored fashion, also send the economy into a recession. Indeed, those expectations seemed accurate over the spring and summer, as job growth slowed, consumers pulled back, household confidence sank. Inflation cooled significantly, rushing towards the Fed’s 2% target.

Hence, the Fed’s priorities understandably shifted from curbing inflation to keeping the job market—and the overall economy—afloat. Even as conditions stabilized during the fall, policymakers thought it prudent to take out insurance against the risk of recession, cutting rates by smaller amounts in November and December. But it soon became clear that the economy was holding up much better than the Fed expected and, critically, that the retreat in inflation hit a wall, remaining stubbornly elevated well above the Fed’s 2% target in recent months.

Unsurprisingly, the mindset of the Fed is changing once again. The latest decision on December 18 was dubbed a hawkish rate cut because it came with a stern message from Chairman Jerome Powell that the path of future rate cuts will be shallower than predicted in September. Powell correctly noted that the economy’s resilience enables policy to move more cautiously, a tacit admission that the aggressive rate hikes in 2022 and 2023 did not inflict as much pain on the economy as expected. Hence, the risk of keeping rates higher for longer has diminished. At the same time, inflation is proving stickier than thought, smoldering rather than simmering, which could be rekindled if rates are cut too far.

As we enter 2025, the lesson from 2024 is that policymakers should remain flexible and forecasters should stay humble, as things can change quickly.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

This newsletter is provided for informational purposes only.

It is not intended as legal, accounting, or financial planning advice.