The One Certainty This Year is — Uncertainty

It would be wonderful to say that the economy started 2025 with a bang, setting the stage for another year of solid market performance. Unfortunately, that’s not the case, as activity-related key data weakened and inflation jumped in January. Thankfully, one month does not make a trend, and it would be a mistake to extrapolate early-year numbers into the future. For one, January’s data are less reliable than in other months. That’s been especially true since Covid, which greatly disrupted seasonal price and spending patterns and has complicated the task of seasonally adjusting new data. For another, January brings unpredictable climate conditions; the presence of devastating wildfires and extreme cold this year made interpreting the data more difficult.

Keep in mind, too, that the onslaught of executive orders and tariff proposals by the Trump administration is still reverberating through the economy. It will take time to process the impact of these rapid-fire directives, and whether they are just a negotiating ploy or firm commitments that result in real changes. But uncertainty can affect behavior; plans can be put on hold, households can either defer or pull forward spending, and, importantly, rate-setting plans by the Federal Reserve can be put in limbo. Indeed, the central bank has already moved to the sidelines, pausing its rate-cutting campaign at the last meeting in January.

There are still compelling reasons to be optimistic about 2025. Most notably, the job market is stable, allowing households to sustain spending. Consumers account for about two-thirds of economic activity, so if they continue to spend, there is little risk that the U.S. will fall into a recession. That’s not the case for other parts of the world, as growth in Europe and China is relatively sluggish and they are facing many of the same uncertain conditions as the United States. Chief among them is the possibility of an all-out trade war, which would dampen an already tepid outlook and have unintended consequences for the U.S., many of which would be negative.

Extensive Tariff Rollout

President Trump took office less than two months ago, but it is hard to identify another post-election period crammed with as many immediate executive actions. As promised in his campaign, Trump is determined to use America’s economic muscle to reset trade relationships and accomplish other non-trade related goals, such as coaxing trade partners to tighten their borders and stifle the flow of drugs to the U.S. To this end, the President’s main tool has been the threat of higher tariffs on the goods Americans purchase from abroad.

As of this writing, the White House is rolling out an eye-opening array of tariffs. All goods imported from China have been hit with an additional 10% tariff; the suspended 25% tariffs on Mexico and Canada are scheduled to be reimposed on March 1st; and a 25% tariff is set to be imposed on steel and aluminum imports from all sources beginning March 12th. Additionally, an official study of reciprocal tariffs, where the U.S. matches the tariffs imposed on it, is due April 1st. The President has also threatened other tariffs, including on the European Union, motor vehicles, and pharmaceuticals.

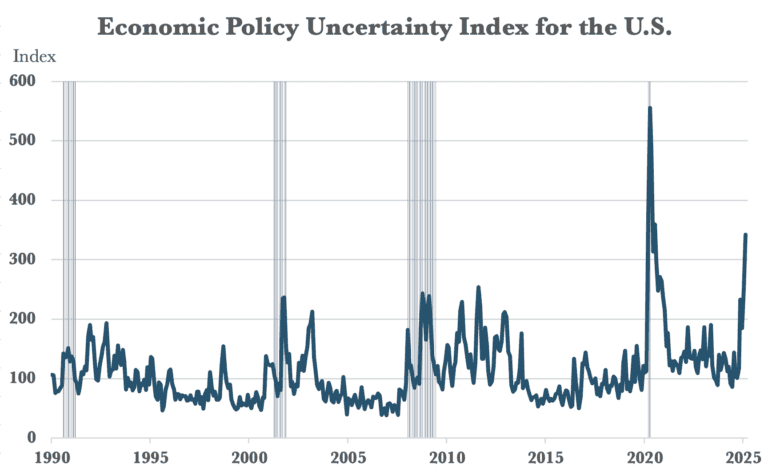

It’s quite possible that some, if not most, of the dizzying array of tariffs will be reduced, postponed, or removed entirely if trading partners meet the administration’s demands. Alternatively, the other nations may respond with hostility and execute retaliatory measures, leading to a destructive trade war that would have unpredictable consequences on inflation and global growth. One thing is sure: the possibilities are broad, and uncertainty is prevalent. An index revealed by the Federal Reserve Bank of Atlanta shows that the current level of uncertainty is higher now than prior to the onset of the past four recessions.

Uncertainty is Problematic

There is an old saying that Wall Street abhors uncertainty. Traders and investors require a reasonable understanding of the policies they will be operating under and only then can they assess how those policies will affect profits, inflation and the revenue drivers of specific industries or sectors. Sometimes those assessments are correct; other times they are not, and investors are rewarded or penalized accordingly. But when the rules of the game are unknown, analysts are hard-pressed to put their skills to use, underscoring their abhorrence of uncertainty. In turn, this fog of uncertainty generates heightened market volatility and increases investment risks on Wall Street.

Main Street also abhors uncertainty, and this is where it can induce real changes in behavior. If businesses are uncertain what their costs will be in the future – in this instance, tariffs specifically – they might put investment plans on hold and freeze hiring. The potential for altered behavior has already appeared in numerous quarterly earnings calls over the past several weeks; that includes the nation’s largest retailer and private employer, Walmart, whose Chief Financial Officer noted that “We are one month into the year, and there’s a lot that we don’t know,” regarding tariffs and how shoppers might react.

Importantly, small firms are more vulnerable to policy uncertainty than their larger counterparts. Those that are reliant on imports have fewer options when trade tensions escalate, as larger corporations can more easily source product from other non-tariffed countries. Furthermore, tariffs present only one type of policy uncertainty; mass deportations represent another. The prospect of mass deportations would cut deeply into the labor supply and pose a major problem, particularly for the construction industry, which is dominated by small employers and is heavily reliant on unauthorized immigrant workers.

Who Let the DOGE Out?

To be sure, resetting trade relationships through tariffs is only one of the top priorities of the incoming administration. Getting a handle on the ballooning fiscal deficit – and reducing the monumental $36 trillion in Treasury debt – is also high on the list, with President Trump and his advisors hoping to cut the red ink dramatically during his term. The revenues expected from tariffs are part of the plan, as that money would be used to pay for the extension of the 2017 tax cuts. However, the main thrust behind the deficit-reducing effort is coming from the spending side of the ledger, as the administration is hoping to slash $2 trillion from the $6.7 trillion in annual Federal outlays.

The responsibility of finding those savings has been given to the newly created Department of Government Efficiency (DOGE). Despite headline-grabbing proposals – eliminating government agencies, slashing federal payrolls, and canceling contracts, among others – very little in the way of savings has so far been accomplished. Importantly, very few budgetary experts believe that so much can be saved without cutting into sacred entitlement programs that most lawmakers are reluctant to touch.

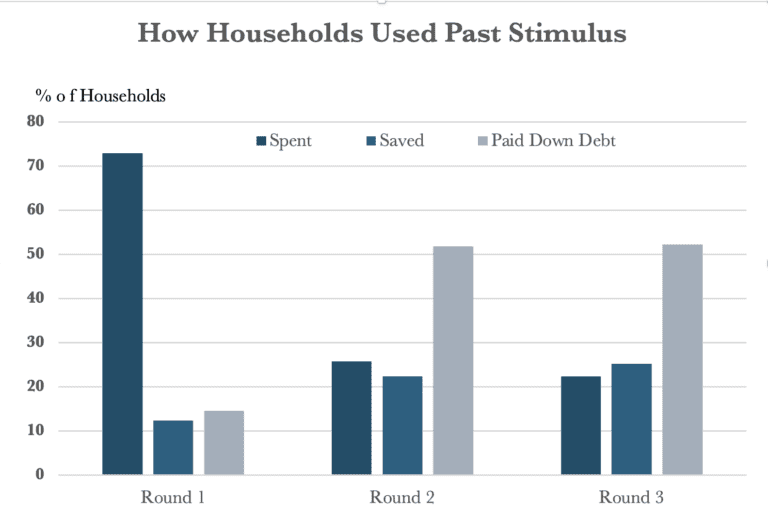

Recently, the administration suggested the potential of a “DOGE Dividend” if the $2 trillion target is met, in which 20% of the DOGE savings would be used to provide a direct payment to taxpayers. The aim is to inject stimulus into the economy that would offset the growth drag that $2 trillion in spending cuts would bring about. However, if the use of previous stimulus disbursements is any indication, most of the estimated $40 billion in dividends (20% of $2 trillion) would be used to pay down debt or saved. Still, if only 25% of the payments were spent, as was the case during the last round of stimulus, with the economy at nearly full employment, the main effect would most likely be to add to inflation and widen the trade deficit, sabotaging a key objective of tariffs.

Cloudy Crystal Ball

Trade and fiscal policies are wild cards in the outlook for 2025 and beyond. The market currently views the proposed full package of tariffs and spending cuts as highly unlikely. But that has not stopped speculation nor stemmed the upsurge in uncertainty that is resonating through the financial markets, corporate board rooms, and households, whose inflation expectations have started to climb sharply. In the latest University of Michigan Survey, household long-term inflation expectations – expected inflation five years out – surged to the highest level in thirty years in February, although political biases played a large role.

Granted, the direct impact from tariffs and fiscal actions regarding spending and taxes would not hit the economy until late this year and 2026. But indirect effects will happen more quickly and their presence may already be felt. Some consumers pulled forward purchases of big-ticket goods to beat price hikes linked to tariffs. Those purchases may have boosted overall spending in December but left a void in January, when retail sales slumped, reinforcing the distortions in the seasonally adjusted data noted earlier. Meanwhile, the increase in inflation expectations may be giving businesses cover to raise prices more than they otherwise might, boosting actual inflation.

Finally, the Federal Reserve has acknowledged that the prospect of higher tariffs is factoring into rate-setting decisions. The decision to pause the rate-cutting campaign had more to do with the ongoing strength in the job market and stubbornly high inflation in recent months. But some officials admit that their subjective thinking of inflation has increased because of the tariffs and reaffirmed their view that fewer cuts are likely than were expected a few months ago. The prospect that interest rates – and hence borrowing costs – are likely to stay higher for longer creates a larger than expected headwind for the economy in the second half of the year. Slower growth and higher inflation is a combination dreaded by policymakers. The Fed has a dual mandate: to pursue maximum employment and maintain a stable, targeted inflation rate. Achieving one side of the mandate is hard enough, but a policy dealing with both when they are moving in opposite directions has rarely been accomplished without causing a recession. Let’s hope the fog of uncertainty clears up soon so one obstacle in the way of a healthy economy in 2025 is removed.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

This newsletter is provided for informational purposes only.

It is not intended as legal, accounting, or financial planning advice.