On the surface, the U.S. economy appears strong. GDP growth is near its short-run potential, unemployment is low, consumer spending is robust, and manufacturing is reviving, driven by AI-related investments in structures and equipment. Based on the strong performance of all key indicators in December, the economy is riding considerable momentum as we enter 2025. Barring an external confidence-shattering shock—such as an escalation of geopolitical conflicts, an oil crisis, or a global trade war that disrupts international commerce—the U.S. economy should perform well in 2025 and once again fare well on the global stage.

However, underneath this surface lies a bifurcated economy, a trend we expect to persist throughout the year. High-income households benefit from several spending tailwinds, including positive wealth effects from past increases in equity and home prices. Since this segment of the population accounts for the majority of U.S. consumer spending, their contribution will be sufficient to keep the growth engine running on most cylinders. Conversely, low- and middle-income households do not reap the benefits of appreciating assets as much. They will remain under financial pressure from previous price increases in food, rent, transportation, and energy.

The perception of the economy also varies depending on employment status. The layoff rate is low, reflecting the tightness of the labor market, and nominal wage growth among job stayers is still around 4% per year, outstripping inflation. However, conditions are challenging for those unemployed or not in the labor force but seeking employment. Hiring has dropped to its lowest rate since 2010, when the economy was still recovering from the aftermath of the financial crisis.

The bifurcation of the economic landscape makes policy decisions more challenging in the coming year. A pro-growth bias in policy could help close the gap between the rich and poor more quickly by creating job opportunities for lower-paid workers. However, this could also heighten inflation, placing a greater burden on lower-income households in the future. Fiscal authorities face similar challenges in tax and spending decisions, as achieving fiscal balance has unequal consequences for the population. Simply put, the overall economy may appear healthy this year, but considerable asymmetries persist.

Who's on First

In the closing months of 2024, monetary policy took center stage as little was done on the fiscal front during the waning days of the Biden administration. The Fed cut rates three times, totaling a full percentage point, between September and December, while congressional efforts were focused on campaigning leading up to national elections. In the early months of 2025, we should see more action on the fiscal side than on the monetary side. The Fed is in a holding pattern following the last rate cut in mid-December, waiting to see how the economy holds up without another rate reduction and whether the inflation retreat, which stalled out in late 2024, resumes.

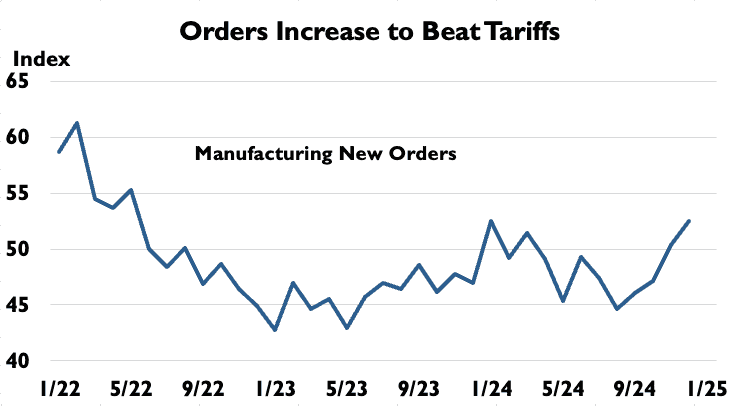

To be sure, major fiscal measures will not be implemented right away, as tax and spending proposals need to go through a grinding process in Congress. However, the proposals themselves could influence behavior and, consequently, the economy. This is particularly the case with President Trump’s signature effort to impose wide-ranging tariffs on China and other key trading partners. It is unclear how much can be accomplished immediately without congressional approval through executive action, but the anticipation of higher tariffs is already prompting businesses to recalibrate spending plans.

Most notably, factory purchasing managers are stepping up orders for equipment and supplies, both from overseas and domestically, to beat the increased price tags that would accompany higher tariffs. Many in the incoming administration believe that higher prices will be avoided because overseas producers will cut prices by as much as the tariff increase to avoid losing sales in the U.S., particularly for products that face domestic competitors. However, the experience during President Trump’s first term belies that notion, as the tariffs imposed on steel, aluminum, washing machines, solar panels, and goods from China, affecting more than $380 billion worth of trade, led to steep price hikes for many of those products.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Will the Fed Respond to Tariffs?

The step up in imports to beat price hikes may provide a short-term growth boost, which would unwind as the economy absorbs the imports and ordering settles down to pre-tariff levels. However, more serious consequences could occur if the Fed believes the growth spike is sustainable, prompting them to keep interest rates higher for longer. This prospect is even more likely if the initial strength, along with the tariff pass-through to consumers, keeps inflation higher than otherwise.

Normally, the Fed does not consider uncertain government policies when making decisions. However, at the December meeting, Fed Chair Powell admitted that some officials on the rate-setting committee were contemplating the administration’s fiscal, trade, and immigration policies. All else equal, the Fed likely believes these policies carry more inflation risk and decided to slow the rapid rate-cutting campaign that began in 2024. Bond traders seem to feel the same way, as long-term interest rates have increased significantly since the Fed started cutting rates in September of last year, although the continued strength of the economy played a large role as well.

While tariffs are the most discussed influence behind inflation concerns, it would be a mistake to overlook the impact that mass deportations could also have. According to the PEW Research Center, undocumented immigrants account for more than 10%of construction and agricultural jobs and nearly as large a share of home health aides. Housing, food, and health care have contributed significantly to the inflation surge in recent years and removing a large chunk of labor in those sectors would intensify pressure on prices, a burden that would fall more heavily on low and middle-income families than wealthier households.

Some Are Falling Behind

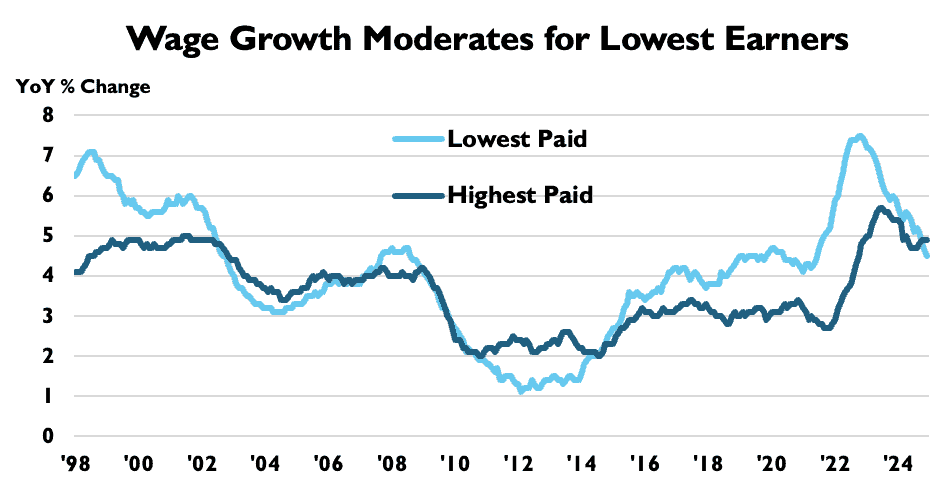

The good news for lower-income workers is that their wages increased faster than those of higher-paid workers during the white-hot job market over most of the post-pandemic recovery. Recall that in 2022 and 2023, the unemployment rate fell to a 50-year low of 3.5%, with two job openings for every unemployed worker when the job market was at its tightest. But that has changed. Hiring slowed in 2024, and the labor supply expanded – thanks in good part to immigration – a combination that loosened labor conditions considerably. By the end of 2024, the ratio of job openings to unemployed workers had fallen to 1.1, essentially balancing the labor market.

However, even as they enjoyed faster pay increases than others, lower-income workers faced steeper price increases, particularly for necessities like housing and groceries, and were forced to go deep into debt to maintain living standards. Now, they are being hit with a double whammy. Wages are slowing overall, thanks to the Fed’s rate-hiking campaign in 2022 and 2023 that weakened the job market, but wage increases for lower-paid workers are slowing even more. For the first time in a decade, workers on the bottom rung of the wage scale received smaller raises than the highest-paid workers.

Fortunately, most workers still have a job and are receiving paychecks, as the unemployment rate is still near historical lows at around 4%. However, the slimmer wage gains for lower-paid workers not only strain their budgets more than those of higher earners but also have significant consequences for the broader economy. Remember, lower-income individuals tend to spend a majority of wage increases, so the smaller raises have an amplified impact on consumer spending.

Small Firms Are Also Hurting

Like wealthy households, medium and large businesses are doing well and are better positioned to weather high interest rates. They have been generating healthy profits, have more pricing power, and have access to capital markets and banks to raise funds. However, small firms, which are the backbone of the economy, face significant challenges. According to the ADP National Employment Report, employment in this sector has stagnant over the past couple of years. Small businesses are under pressure from high interest rates, elevated costs, a difficult lending environment, and softening sales. Moreover, small businesses have relatively less access to capital markets and rely more heavily on banks for funds.

As a result, they are more vulnerable to tightening lending standards and high borrowing costs, which are closely linked to Fed rate increases. This becomes particularly problematic when small firms encounter difficulties and cannot raise funds to avoid bankruptcy. Not surprisingly, small business bankruptcy filings, as indicated by Chapter 11 Subchapter V filings, are surging. Subchapter V filings in 2024 were 9.8%higher than in 2023 and 44.2% higher than in 2022. It’s important to note that there was a surge in business formations after the pandemic; with more business births come more business deaths as the survival rate across industries declines over time.

This is where the Fed could find itself in a bind. The three rate cuts last year provided some relief for small firms, and hopes were high that several more cuts would follow this year, beginning as soon as January. However, due to stickier inflation late last year and the economy’s sustained strength, further rate cuts have been delayed and the number of expected cuts reduced. While sticky inflation could justify a prolonged pause in rate cuts, this could risk imposing an additional burden on small businesses and, by extension, the labor market. Simply put, monetary policy is a blunt instrument, and the prospect of rates staying higher for longer may well be necessary to keep inflation in check. Hopefully, the Fed will weigh the balance of risks appropriately and guide the economy toward slower but sustainable growth in 2025. However, the presence of a bifurcated economy will likely continue for a while longer.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

This newsletter is provided for informational purposes only.

It is not intended as legal, accounting, or financial planning advice.