Reflections on the U.S. elections are ongoing and will likely dominate the media for some time. With the polls now closed, all eyes are on the likely impact of the incoming Trump administration on the U.S. economy. Most commentators believe that the prospect of higher tariffs, massive deportations, and broadly based lower taxes are inflationary. However, bold campaign proposals are often watered down before becoming actual policies. Moreover, viewing a president’s agenda in a vacuum is a mistake. Higher tariffs invite retaliation by trading partners, leading to unintended consequences such as higher business costs, lower profits, and eventual job cutbacks.

Aside from inducing heightened volatility in the financial markets, investors always loathe uncertainty. The full impact of Trump’s signature proposal and higher tariffs would not be felt until late 2025 and 2026. In the meantime, the incoming administration will inherit an economy still heavily influenced by policies from the Biden regime – good and bad – and the legacy of the Federal Reserve’s recent policies. While many fear escalating tensions with other nations, the U.S. economy remains the envy of the world, having emerged from the Covid recession much more vital and, despite domestic angst over prices, with lower inflation.

Barring sudden external shocks, that outperformance should continue. The tailwinds driving the U.S. economy are numerous and still powerful. The increase in productivity last year is not a flash in the pan but something that should endure. This, in turn, enhances the economy’s growth potential and helps curb inflation. Consumers still have significant spending firepower generated during the post-Covid years, and fiscal measures unleashed during the Biden administration, such as the Chips Act, are poised to launch a boom in business capital spending. To be sure, the economy faces risks. The prospect of a contentious political environment could heighten policy uncertainty among traders, risking a severe correction in financial markets. This could take a toll on household wealth and undercut business confidence, resulting in less investment spending and reduced hiring, if not outright job cuts. Perhaps the only certainty is the heightened uncertainty that will linger until the new administration’s policies come into more precise focus.

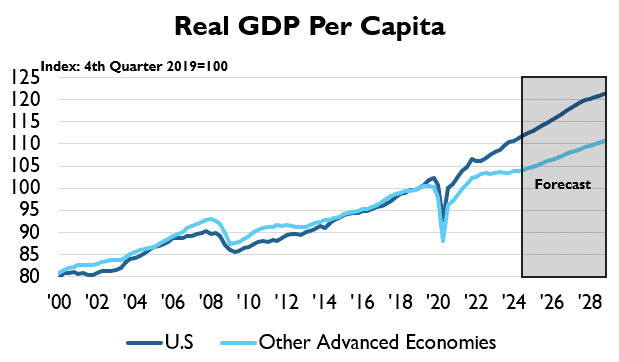

U.S. Outperforms

The last 15 years can generally be characterized as a period of American exceptionalism. U.S. per capita GDP growth was the third strongest among advanced economies in 2023 and is poised to be among the best performers again this year. Even setting aside the prospect of expansionary fiscal policy, U.S. exceptionalism is expected to endure next year despite heightened policy uncertainty and financial market volatility. Next year, the key drivers for growth in the U.S. are consumer spending and business investment in equipment, both benefiting from strong tailwinds.

The recent upsurge in productivity growth isn’t a flash in the pan. This trend should continue thanks to robust business spending on research and development, continued advances, broader applications of artificial intelligence, and ongoing efforts to cut labor costs. Stronger productivity growth will keep the U.S. economy’s potential growth rate elevated next year, along with an increase in the labor force.

The Trump administration’s stance on immigration and trade may well be a drag on GDP growth down the road, but it won’t be a major factor in 2025, helping ensure that the U.S. economy’s outperformance will continue. Another reason the U.S. economy has outperformed other advanced economies is the aggressive expansion of fiscal policy during the pandemic. Importantly, not all the deficit spending went toward stimulus payments, which clearly boosted consumer spending over the past three years. While most of those funds have been spent, the bipartisan infrastructure bill, Inflation Reduction Act, and CHIPs Act will continue to support business investment and productivity growth for years to come.

Big Lift from Business Investment

No doubt, consumers have been the main engine of growth in recent years, thanks to stimulus payments and accelerated wage growth linked to a historically tight job market. A lesser but growing adjunct to consumer spending should kick in next year and sustain the U.S. economy’s exceptional growth on the world stage. Simply put, the rapid growth in investment in nonresidential structures, particularly in manufacturing, will be a tailwind for equipment spending next year. There is a roughly two-year lag between an increase in factory construction and the associated boost to equipment investment. The equipment cycle will kick in next year and into 2026 as real investment in manufacturing structures this year is on track to be the largest in the post-war era.

What’s more, companies are in a good position to fill these new structures with the necessary equipment. Strong profits, healthy balance sheets, lower borrowing costs, and easier lending conditions indicate that businesses will have the necessary funds to finance the expenditures associated with growth. In addition to these positive fundamentals, the fiscal environment should also give a hefty boost to capital spending. Republicans swept the White House and Congress on Election Day, and the outlook for equipment spending is sensitive to the presumed GOP trifecta fiscal policies.

The party’s agenda includes reviving the full expensing of qualified business equipment, which would lend meaningful support to capital investment. It appears that Republicans are in favor of repealing most electric vehicle tax credits granted under the Inflation Reduction Act (IRA) but prefer leaving the remainder of the clean energy tax credits untouched. In August, 18 House Republicans sent a letter to House Speaker Mike Johnson opposing a full repeal of the IRA’s clean energy tax credits, citing the investments in the energy sector since its passage. The IRA will benefit business investment most directly through its tax incentives for domestic production of solar panels, wind turbines, battery components, and critical minerals. The climate law will also have positive spillover effects on electrical equipment spending as the new renewable energy supply is connected to the existing power grid.

Consumers Still Chugging Along

Like fine wine, the American consumer gets better with time. A few months ago, most economists thought households were running out of fuel, having spent their stimulus checks and exhausted the savings cushion built up during the pandemic and its aftermath. Many believed this pullback in spending risked putting the economy on the cusp of a recession late this year. Indeed, the jumbo half-percent rate cut by the Fed in September, followed by a smaller quarter-point cut in early November, aimed to prevent such an occurrence by lowering borrowing costs for consumers and, more broadly, easing the growth-dampening brake that high interest rates were imposing on the overall economy.

While many felt the Fed’s move was overdue, the recession risk implied by an exhausted consumer turned out to be a false alarm. Revised data revealed that households had more income and savings than previously thought and were more than willing to spend those funds. Instead of rolling over in the waning months of the year, consumer spending jump-started what is shaping up to be a festive holiday shopping season. Retail sales in September and October were much stronger than expected, prompting economists to upgrade their growth forecasts for the fourth quarter. The widely followed Atlanta Federal Reserve GDP tracking model is pegging a growth rate of 2.6 percent (as of November 16) for the quarter, which would be almost spot-on with the above-trend 2.8 percent pace in the second quarter.

However, unlike the support for business, the fiscal environment is not shaping up for consumers either. True, lower taxes would put more money in people’s pockets. However, it is likely lawmakers will be primarily focused on extending the tax reductions due to expire in 2025 rather than implementing additional tax cuts. Meanwhile, consumers, particularly low- and mid-income households, are vulnerable to tariffs, which are inflationary and will bite into real disposable income. Importantly, the higher deficits that are certain to occur will keep market interest rates higher than otherwise and may well slow the Federal Reserve’s rate-cutting campaign. Investors are already pricing in fewer rate cuts next year than previously expected.

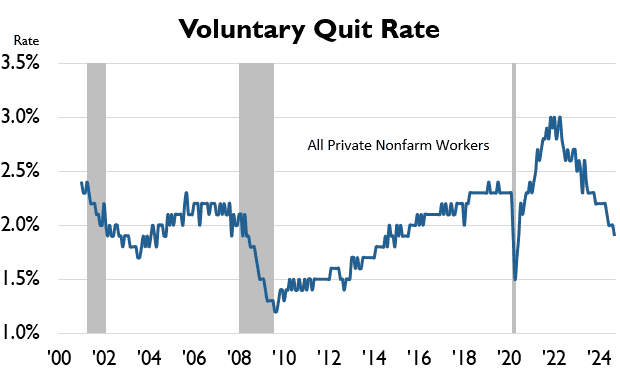

Warning Signs

The biggest risk that could throttle the economy’s growth engine next year would be a collapse in the job market. That’s unlikely to happen unless, as noted earlier, some confidence-shattering external shock sends tremors through the business community. Barring that, the fundamentals supporting a healthy labor market remain intact. Consumers are still spending, propelled by rising wages and strong balance sheets. Businesses are still hiring as both profits and sales hold up well. And while tariffs may be a drag on growth down the road, they are giving a jolt to activity over the near term, as many companies step up orders from abroad before tariffs kick in.

That said, it would be a mistake to ignore emerging signs of weakening labor conditions. There are far fewer job openings than earlier this year, workers are choosing to stay put rather than quit for jobs elsewhere, reflecting less confidence in finding one, and while layoffs are low, unemployed workers are taking longer to find a job. Simply put, under the hood of the historically low unemployment rate, conditions are starting to stagnate. That’s not necessarily a bad thing; the job market was overheated, and a cooling-off is needed to help bring down inflation. If the Fed reads the signs correctly and keeps the job market from further weakening without stoking an inflation rebound, the U.S. economy’s exceptionalism will endure. But the Fed will take a back seat to policymakers in the White House and on Capitol Hill in the coming months, and the hope is that they can avoid a messy rollout of policies that would upend what is looking like a bright future for the U.S. economy.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

This newsletter is provided for informational purposes only.

It is not intended as legal, accounting, or financial planning advice.