What Is New with IRA Contributions?

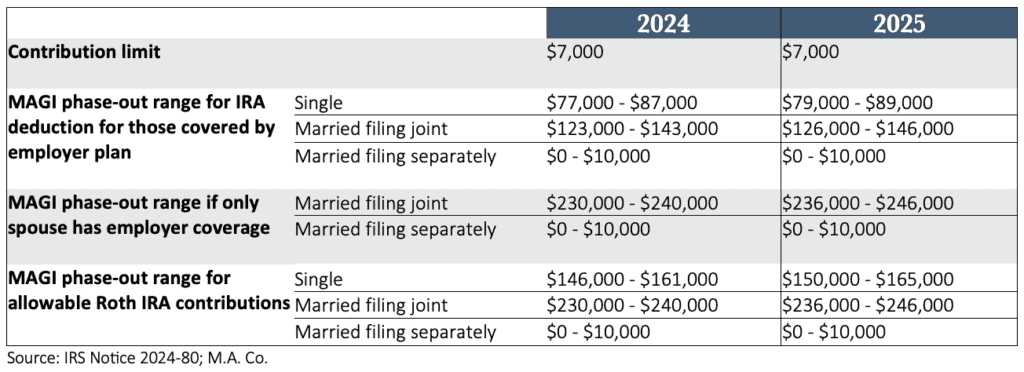

Since 2020, individuals of any age with earned income have been eligible to contribute to a traditional IRA, eliminating the previous age limit of 70½. It’s important to note that earned income excludes income from investments, Social Security, pensions, or gifts. Additionally, the age for beginning required minimum distributions (RMDs) has been increased to 73, allowing more time for retirement savings to grow tax-deferred. For 2024 and 2025, the IRA contribution limits remain unchanged at $7,000 for individuals under age 50 and $8,000 for those 50 and older, which includes a $1,000 “catch-up” contribution. While the catch-up contribution will eventually be indexed for inflation, no adjustments have been announced for the 2025 tax year

As an IRA account holder, you are likely already familiar with the value of maximizing your contributions each year. With the 2024 tax filing deadline approaching, now is the perfect time to ensure you take full advantage of available opportunities. Here is a look at key updates and reminders to help you make the most of your IRA.

Timing Matters

You have until the tax filing deadline in April 2025 to contribute for the 2024 tax year. To optimize your retirement savings further, consider making your 2025 contribution early in the year to take advantage of the maximum tax-deferred growth potential.

Deduction and Income Considerations

While contributing to an IRA is straightforward, qualifying for a deduction depends on your specific circumstances. If you are not covered by a workplace retirement plan, you can deduct your entire traditional IRA contribution, regardless of your income. However, if you or your spouse is covered by an employer-sponsored retirement plan, the deduction for your traditional IRA contribution phases out as your modified adjusted gross income (MAGI) increases. For individuals who exceed the deductibility thresholds, a Roth IRA can be an attractive alternative. Although contributions to a Roth IRA are not tax-deductible, qualified withdrawals in retirement can be entirely tax-free, offering significant long-term benefits.

Key IRA Boundaries

Plan for Success

Now is a great time to review your contribution strategy to ensure it aligns with your retirement goals. Whether you’re considering a Roth IRA for its tax-free growth potential or maximizing your traditional IRA contributions for the year, we’re here to help.

Contact your advisor to discuss how these updates may impact your overall financial plan. Together, we can maximize your retirement savings.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

This newsletter is provided for informational purposes only.

It is not intended as legal, accounting, or financial planning advice.