The holiday shopping season has officially kicked off, and a less festive Santa than we have seen in recent years will likely be coming down the chimney. For sure, the nation’s collective stockings will not be filled with coal, but the presents will be less plentiful and generous than in 2022. We don’t expect consumers to zip up their wallets and purses entirely, but they are running out of the fuel that pumped up spending last year and the year before. Job growth is slowing, the pandemic-era excess savings are mostly depleted, banks are tightening credit, student loan payments have restarted, and borrowing costs have spiked.

We have noted in the past that the downbeat mood of households does not always translate into weaker spending decisions. That divergence was strikingly evident in the third quarter when consumers went on a veritable spending binge despite expressing deep dissatisfaction with the economy’s direction. However, they are behaving more like they feel, as retail sales in October fell for the first time since March. The National Retail Federation expects holiday sales in November and December to rise by 3-4% from last year, weaker than the 5.4% gain in 2022 and the blistering 12.7% in 2021.

The good news is that consumers are getting some relief on the inflation front. Retail inflation plunged from 9.1% in March 2022 to just over 3% this October, the most pronounced decline outside of a recession since the early 1950s. Wage growth is also slowing but not as rapidly, so paychecks are going a longer way. That, in turn, should keep a floor under spending. However, the Federal Reserve believes wages are still growing too fast, thereby preventing inflation from retreating to their 2% target. The risk is that the central bank will keep interest rates higher for too long, bringing on an unnecessary recession. Hopefully, the Fed does not shape policy decisions on an unrealistic timetable. When wage growth does slow enough, it may be too late for the Fed to cut rates to ward off a recession.

Higher Speed Limit

The financial markets have been on a tear since early November when the Fed decided to keep their key policy rate unchanged for the third consecutive meeting. The Fed did not change their forecast of one more increase, which they predicted over the summer. Still, recent comments by Chair Jerome Powell and many of his colleagues strongly suggest that the final hike is now in the rear-view mirror unless the inflation decline stalls out or, worse, reverses.

The most interesting aspect of the Fed’s decision to put rate hikes on hold is that it comes on the heels of a gangbuster growth rate for the economy, as real GDP (net of inflation) surged by an eye-opening 5.2% annualized rate in the third quarter, the strongest since 2021 and way above the economy’s potential growth rate of approximately 2%. Nominal GDP growth of 8.9% was the highest since 2003 (ex-Covid reopening). Historically, when the economy grows faster than its output capacity, inflationary pressures increase and spur the Fed into demand-curbing rate hikes. That backdrop stoked the inflation surge in 2021 and 2022 when trillions of dollars in stimulus payments boosted demand while global supply constraints suppressed output. Although demand is slowing now, consumer inflation expectations are rising, and actual inflation remains higher than the Fed’s 2% target. So, what’s behind the Fed’s newfound patience?

The answer is that the Fed thinks the economy has undergone a significant transformation that allows inflation to continue to recede even if growth exceeds its long-term trend. Indeed, that’s precisely what occurred in the third quarter when, to the surprise of many, torrid growth did not prevent inflation from falling. Simply put, the economy’s potential growth rate – its speed limit – also ratcheted up, more than matching the surge in demand. That’s because the supply constraints that restrained output and growth are unraveling: labor shortages eased as people returned to the workforce, bottlenecks cleared up, easing product shortages, and productivity increased. These conditions remain in place and could reasonably act to reduce inflation for a while longer.

Soft Landing Hopes Improve

The Fed’s recognition that the economy’s increased growth potential could suppress inflation is a striking about-face. Until recently, policymakers thought that only a severe cutback in growth and, by extension, a weaker job market would bring inflation down. Although not explicitly stated, it was generally assumed that Fed officials would accept a recession as collateral damage in the anti-inflation fight, hoping that any downturn would be mild. The Fed was not alone in this thinking. Wall Street and most economists looked at the historical record of Fed tightening cycles. They were just as convinced that a downturn was inevitable, particularly given how aggressively rates have increased since March 2022.

However, following a record 13 consecutive months of declining core inflation, a consensus is forming that the Fed can conquer inflation without causing a recession, thanks in good part to the economy’s expanded output capacity, which allows supply to meet a sustained increase in demand. This prospect, known as a soft landing or, more recently, “immaculate disinflation,” is also gaining acceptance in the financial markets, spurring a strong rally in stock prices and a decline in bond yields. Even the Fed have come around to this thinking, with Chair Powell noting that a recession is no longer the default option. But he also notes that wringing the last mile out of inflation from 3% to 2% will be more of a struggle unless wage increases slow more sharply.

Still, the inflation doves argue that if price increases can be slowed from 9% to 3%, there is no reason another 1% can’t be wrestled out of the system without inducing more economic damage than necessary. In their eyes, since the unusual pandemic-related shocks that suppressed output and boosted demand are unwinding, it is only a matter of time before inflation returns to pre-pandemic levels. This group understandably believes that the Fed should start cutting rates soon before the pain on housing and other rate-sensitive sectors intensifies, sending the broader economy into an avoidable recession.

Patience Not Unlimited

Undoubtedly, the Fed will keep rates unchanged at their meeting in mid-December, if only because the disinflationary trend is still firmly in place and most officials want more time to assess how past rate increases are playing out. It is also what investors expect, and the Fed rarely takes moves that would disrupt market conditions unless it wants to send a clear message to change investor expectations. The current message is that it will hold off on another rate increase for now, but it is not even considering cutting rates.

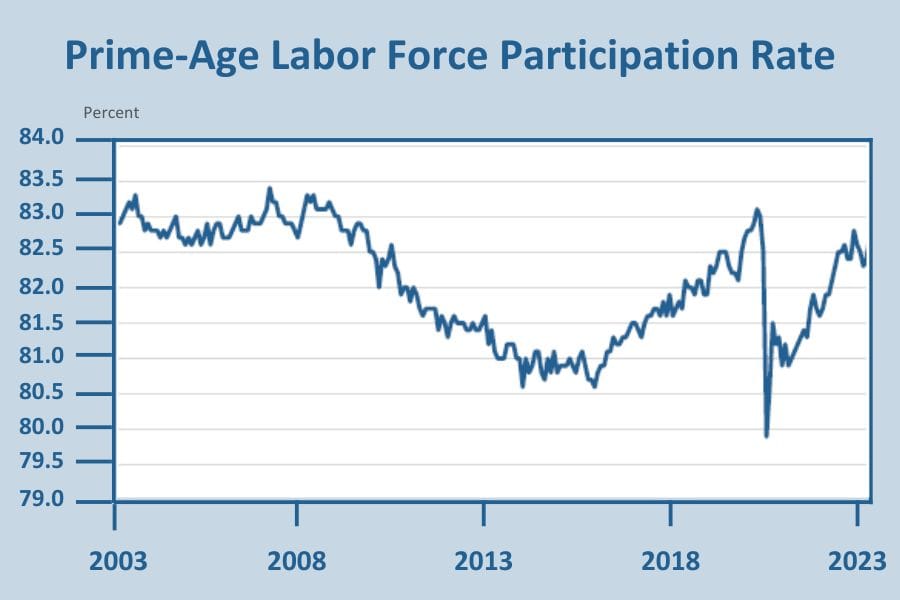

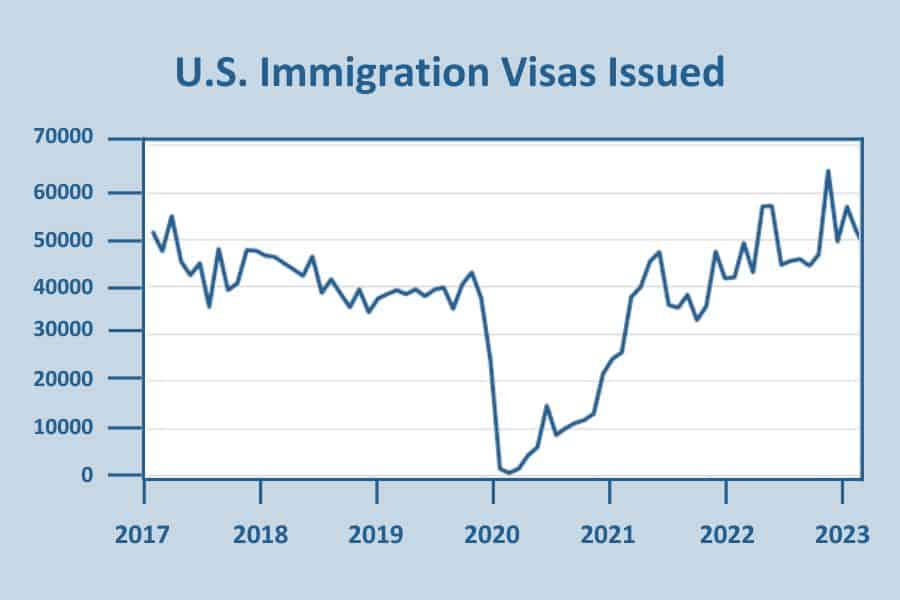

That said, the Fed’s patience in holding rates steady is not open-ended. If the economy and the job market continue to chug along faster than normal, it will be hard to see more of an inflation retreat. After all, the forces that pumped up the economy’s growth potential will not be around much longer. Returning workers and a surge in immigration sparked a rebound in the labor force – relieving worker shortages – but both have reached their limits. The labor force participation rate of prime-age workers is above its pre-pandemic peak, and the administration is cracking down on immigration. Indeed, the number of visas issued by the government fell by almost 50% over the past six months.

Meanwhile, supply chains have been fixed, and goods flow freely to stores and warehouses, where inventories are mostly back to normal. Hence, the production boost aimed at meeting a huge backlog of demand for goods built up during the pandemic no longer exists. Moreover, the cushion of excess capacity that enabled factories to ramp up production to meet demand is virtually gone. Goods-producing industries are operating at a higher percentage of capacity now than at the peak of the 2010-2019 expansion.

Will the Fed Pivot in Time?

Hence, any hope for a soft landing will depend on how well the pilot, namely the Federal Reserve, can bring demand more into balance with the economy’s speed limit, which is poised to lose the temporary influences that pumped up its growth over the past year. The challenge is determining what level of interest rates would bring about that equilibrium and how long to keep it there. To their credit, the Fed hit the pause button in July to gauge the impact previous rate increases are having, recognizing that there are lagged effects that still have not played out.

Many borrowers, for example, are still paying the low rates obtained on loans taken out two or three years ago. The lucky ones are homeowners who locked in those rates for up to 30 years. However, people with credit card debt face record interest rates on their unpaid balances, and delinquencies are rising, particularly among lower-income borrowers. Until recently, pandemic savings helped cover financing costs and were used to pay down a big chunk of outstanding debt. But those savings are mostly depleted even as credit card borrowing has ramped up. Meanwhile, the moratorium on student debt repayments has ended, which will further squeeze the budgets of 40 million borrowers.

Hence, the lagged effects of the Fed’s rate hikes over the past 19 months are starting to kick in, and the drag on consumer spending should become more pronounced in the coming months. Whether the setback in retail sales in October is an early sign of the impact remains to be seen. Consumers may have taken a breather after a torrid spending spree in the third quarter. But with savings diminished and borrowing more costly, households will rely more on jobs and wages to sustain spending. Both are slowing, which should reinforce the unwinding of pandemic shocks to cool off inflation over time.

The risk is that the Fed, who does not see inflation falling to 2% until 2026, will keep rates elevated for too long, leading to a hard landing for the economy. The financial markets are currently pricing in Fed rate cuts starting in the spring of 2024, far earlier than the timetable set by policymakers. It’s unlikely that inflation will be much closer to 2% by then, and Fed officials fear easing policy prematurely before inflation is conquered. The economy may adjust to the higher rate environment and stay afloat, but history indicates that it is hard to stop once slowing growth starts to drive up unemployment. Hopefully, the Fed will take their foot off the brake in time to avoid a recession.

If you are a Legacy client and have questions, please do not hesitate to contact your Legacy advisor. If you are not a Legacy client and are interested in learning more about our approach to personalized wealth management, please contact us at 920.967.5020 or connect@lptrust.com.

The information contained herein is for informational purposes only and does not constitute a recommendation or advice. Any opinions are those of Legacy Private Trust Company only and represent our current analysis and judgment and are subject to change. Actual results, performance, or events may differ based on changing circumstances. No statements contained herein constitute any type of guarantee, nor are they a substitute for professional legal, tax, or other specialized advice.